I export beauty and therapy equipment every week, and I learned that payment terms decide both risk and speed—get them right, and projects move; get them wrong, and cash or cargo gets stuck.

Suppliers typically accept telegraphic transfer (T/T wire), letters of credit (LC), and sometimes PayPal or credit cards for small amounts. Wire is the default, not always the “safest,” just the most practical. Open-account terms are negotiable for proven buyers. The best structure matches order value, relationship, and logistics timing.

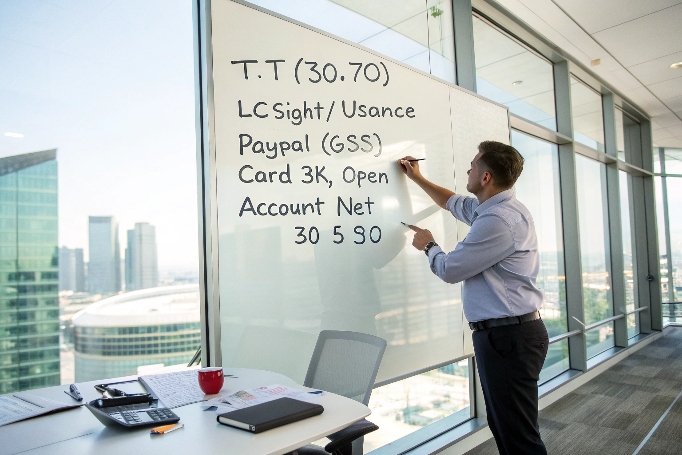

Clear payment design reduces risk for both sides and keeps production, inspection, and shipping on schedule. The sections below explain each method, show common structures by order size, and give negotiation playbooks that work in real deals.

Do suppliers accept credit card payments?

I accept cards for small pilot orders because it helps new clients move fast without bank paperwork, but cards are not built for five-figure capital equipment.

Yes, many suppliers accept credit cards for low-ticket amounts (often under $1,500–$3,500). For larger values, card fees, chargeback risk, and processor limits make cards impractical. Wires, LC, or PayPal (Goods & Services) are more common once the invoice exceeds a few thousand dollars.

Credit cards are great for speed. Authorization is instant, and new buyers gain confidence. However, interchange fees can exceed 3%, which erodes tight hardware margins. Processors may flag international, high-value, or medical-device transactions. Some factories cannot settle foreign cards or lack merchant accounts. For bulk orders, the card limit blocks payment scheduling tied to quality control milestones (e.g., balance after pre-shipment inspection). A hybrid approach works: card for samples, fixtures, or training; wire/LC for production units. Distributors sometimes use virtual cards 1 for small recurring parts orders while keeping capital goods on bank rails.

Is wire transfer the safest option?

I recommend wires for most B2B orders because they are predictable, traceable, and work with milestone payments; “safest,” though, depends on who carries the risk.

Wire transfer (T/T) is the most common and operationally simplest method. It is reliable, but it shifts risk to whichever party pays first. For new relationships or big tickets, combine T/T with safeguards: deposits + inspections, escrow, or a confirmed LC for the first deal.

Wire supports standard structures that align with production and quality events. For example, a deposit funds materials, while the balance is paid after pre-shipment inspection (PSI) and before pickup. Some trading companies allow balance “against copy of Bill of Lading 2,” but most manufacturers require balance before cargo leaves. To strengthen wires, buyers add third-party inspections, factory test videos, and serial-number packing lists before releasing the balance. Escrow or trade assurance platforms 3 add buyer protection but may not be available for customized medical devices.

Also verify the supplier’s SWIFT code 4 and beneficiary name match on invoices to avoid payment diversion scams.

Can open account terms be negotiated?

I grant terms to repeat buyers with consistent volumes, because predictable demand lowers my risk and factory cash strain.

Yes, open account (Net 30–90) is negotiable for buyers with strong trade references or annual spend thresholds (≥$100k–$150k). If a supplier will not start the clock at goods receipt, they may accept terms counted from the Bill of Lading (vessel departure) date. Trade credit insurance or bank-backed instruments can unlock terms.

Open account terms 5 are the most cash-friendly for buyers and riskiest for suppliers. To make them work, suppliers often request financials and references, and sometimes a standby letter of credit (SBLC) 6 or credit insurance. A practical compromise is BL-date Net 30/60/90, which limits exposure. Another path is payment on delivery of documents—D/P documentary collection 7—cheaper than an LC yet safer than pure open account.

Do suppliers accept PayPal or LC?

I use both, but for very different reasons: PayPal for speed and buyer protection on small items; LC for bank-level risk control on large, formal shipments.

Yes. Many suppliers accept PayPal for small invoices (samples, spare parts, training). For larger orders, fees and dispute rules make PayPal less attractive. Letters of Credit (LC) are widely accepted for high-value or first-time orders; they reduce default risk but add banking fees and document work.

PayPal is convenient, with buyer protection and fast settlement, but it brings high fees and strict dispute rules. Suppliers may price-in the fee or cap the amount. Letters of Credit (LC) are classic for international machinery; the ICC explains mechanics in its LC guide 8. For cash-flow relief, a time-deferred usance LC 9 provides terms while keeping supplier security.

To speed compliance, align your LC wording with UCP 600 rules 10 so banks process documents smoothly.

Conclusion

Use cards or PayPal for small, urgent items; use T/T with inspections for standard POs; use LC for large or first-time buys; and negotiate BL-date Net 30–90 once trust and annual volume justify it. Structure beats guesswork, and good documents keep cash and cargo moving.

Footnotes

1. Stripe guide to virtual cards for secure supplier payments. ↩︎

2. Investopedia explanation of the Bill of Lading in trade. ↩︎

3. Alibaba Trade Assurance overview for buyer protection. ↩︎

4. Wise.com article explaining SWIFT codes and bank verification. ↩︎

5. U.S. trade.gov guide to open account payment methods. ↩︎

6. Investopedia resource on standby letters of credit (SBLC). ↩︎

7. Trade.gov overview of documentary collection payments. ↩︎

8. ICC guide to letters of credit and document handling. ↩︎

9. CFI article explaining usance LCs for deferred payment. ↩︎

10. ICC reference for UCP 600 documentary credit standards. ↩︎